For most of the last decade, buying a new car cost the average American worker roughly 33 to 36 weeks of income, a figure that felt stable if not exactly comfortable. Then came the Biden Presidency and its unusual market situation that pushed that number to a painful peak of over 42 weeks of required earnings by early 2023.

Today, the Cox Automotive/Moody's Analytics Vehicle Affordability Index has fallen back to 35.1 weeks as of March 2026, lower than it was during Obama’s second term. Present-day economic policies are offering genuine relief to car shoppers who endured one of the most difficult buying environments in recent memory from early 2021 to late 2024.

The graph at the top of our page is from a Cox Automotive report published this month. We simply overlaid the presidential terms onto it. As you can see, of the four presidential terms shown, President Trump's first term was the period during which shoppers enjoyed the best level of affordability when it comes to buying a new car. During nearly all of this period, the average new vehicle cost workers less than 34 weeks of earnings. For a very long span in the middle of that presidential term, the number of weeks required to buy the average new vehicle dipped close to 32 weeks.

During most of President Obama’s second term, the required weeks were above 34, and throughout Biden’s term, they were never below 34. In fact, during President Biden’s term, the number of weeks of wages required to buy a new vehicle spiked to over 42 weeks. In President Trump’s current term, vehicle affordability improved, then dropped to about 35 weeks of earnings.

Why Measure Vehicle Affordability In Weeks of Wages?

There are a few good reasons why using the affordability index’s unit of measure of weeks of earnings is handy. First, it helps to provide an easy-to-understand metric. We often publish stories that try to explain to readers that vehicle costs are not actually going up; when the devaluation of the dollar is factored in, prices are slightly declining. Like this one that explains how a Honda Civic today costs less than in 1993. We’re not sure we do the best job of explaining the concept of real dollars versus inflation-adjusted dollars, so just using “weeks of your pay” seems to make good sense. Here is what Cox and Moody say about the index.

The Cox Automotive/Moody’s Analytics Vehicle Affordability Index (VAI) is updated monthly using the latest data from government and industry sources, including key pricing data from Kelley Blue Book, a Cox Automotive brand. This important industry measure will be released at mid-month to indicate if the prices paid for new vehicles are moving out of consumers’ financial reach or becoming more affordable over time.

Don't Confuse Overall Vehicle ATP with the Cost of Affordable Car and Crossover Models

Cox and Moody use the average transaction prices of vehicles in their reporting, which makes sense. However, the average price of vehicles overall is much higher than that of compact cars and crossovers. Here is a handy group of five segment price averages to help illustrate how vastly different the overall average is from affordable cars:

- Compact SUV: $37,055

- Subcompact SUV: $30,612

- Compact car: $27,469

- Overall Vehicle ATP: $49,275

As you can see, a compact car is roughly half the cost of the average vehicle in America. This is simply because the average price of a new truck is over $65K, and many luxury segments have ATPs dramatically higher than those of mainstream models of the exact same size that offer the same performance in daily driving. These high-priced vehicle models skew the overall average dramatically.

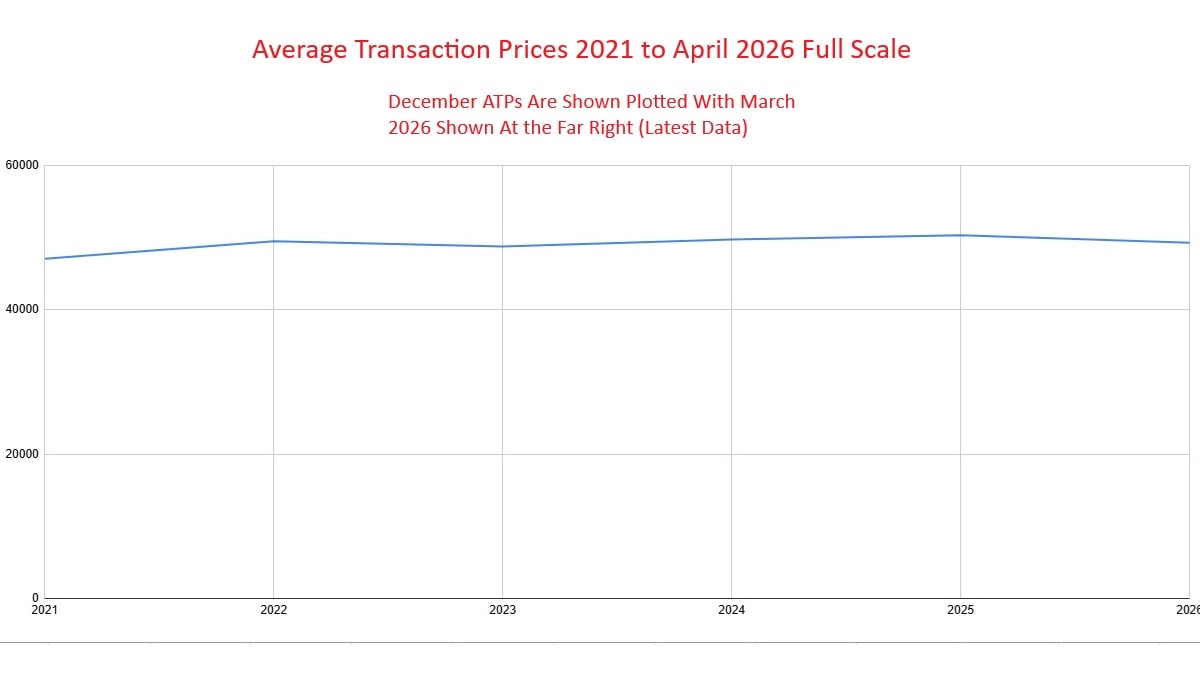

Media groups love to torture the data each month to create fear, uncertainty, and doubt stories that decry the horrors of average vehicle prices. They are very creative. Factually, ATPs have been stable for many years, as our full-scale graph above shows. Here are some facts about average prices we selected from Cox’s latest data published in April.

1) Average transaction prices were higher in December 2022 than in any month in 2026.

2) Average transaction prices in March were over $1,000 lower than in December of last year.

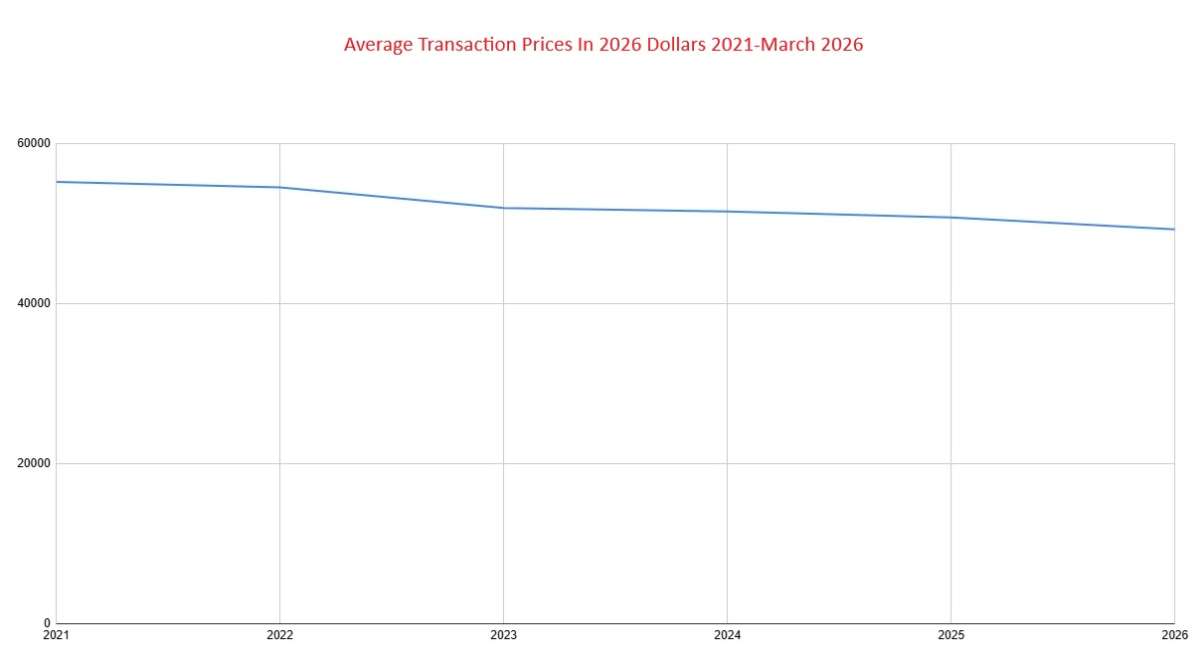

3) Adjusted for inflation, ATPs have fallen steadily for years - even if you include trucks and luxury models. (see graph below)

Salary Increases Are Outpacing Vehicle Price Increases

Now let’s talk a bit about that metric we used above, average American weekly earnings. Rather than offer an opinion on this, let me simply cut and paste some conclusions that Cox published in its recent update:

1) New-vehicle affordability improved in March for the fifth straight month.

2) The average transaction price (ATP) fell 0.1% month over month, while household income rose 0.3%.

3) ATP was higher by 3.5% year over year, while income increased 3.9% over the same period—suggesting income growth is outpacing vehicle price gains.

4) The median number of income weeks required to purchase a new vehicle in March fell to 35.1 weeks from 35.4 weeks in February and 35.4 weeks last year, highlighting continued improvement in affordability.

Many Americans assume that wages are not keeping pace with inflation. This makes sense if you stop and think about it. Americans don't get raises on a weekly or monthly basis. Raises in pay usually come either annually, not at all, or as a jump in compensation with a promotion or a job change. However, inflation can change moment by moment, and the media knows this. They find any scary data they can to constantly remind readers that “prices have gone up!” Well, of course they did. It’s official U.S. Federal Reserve policy that they do. The constant F.U.D. stories have the desired effect, though. Be told once you are getting a raise, but 50 times that prices went up, and it is easy to assume the sky is falling. Even if it’s not.

Finance Rates and Habits Can Impact Affordability Dramatically

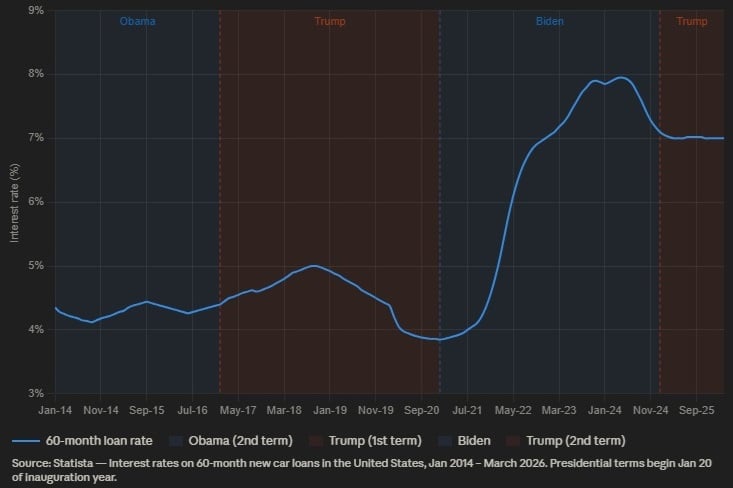

Thus far, we’ve focused on the vehicle's purchase cost relative to average new-vehicle prices. However, there is another big part of the cost of a vehicle to the actual owner. Many buyers finance their new car through the dealer, a bank, or a credit union, and the cost of financing varies widely from year to year and from presidential term to presidential term.

You may have heard the news that President Trump is battling the Fed right now to force interest rates lower. Whether this is a good idea or not is definitely debatable, but the reason he is having the fight is not. President Trump knows that high interest rates cost consumers immense amounts of money on car loans and homes. So, he wants the rates to be lower. Here is a handy graph of interest rates I pulled from Statista and overlaid with Presidential terms.

Although I am an expert on automobiles, I’m not the best source of vehicle financing information. But I know the guy who is. His name is Kamil Kaluski. Unlike me, he’s a “real” engineer. I’m an engineer in recovery. His math skills are better than mine, and better kept up to date. He published a great story this week showing how current interest rates and financial habits are making vehicles less affordable. If you want to learn more and hear a different perspective, I hope you will read his breakdown in Autopian.

I don't finance my vehicles, and when I was younger and had to, I purchased very inexpensive new or pre-owned cars and either paid cash or paid off the auto loans early and aggressively to avoid finance charges. However, I recognize I’m an odd duck this way, and many good people do finance vehicles, so please read what Kamil says. I will not steal his thunder, but here are a couple of key takeaways from his work:

1) The average monthly finance payment, which has climbed to $806, up $125 since 2022. Adding to the insanity is the fact that almost 20% of buyers now have monthly payments over $1000.

2) 72-month loans account for 40.5% of all sales, up 4.1 percentage points since March 2019. 13% of buyers are signing for loans of 84 months or longer.

Vehicle affordability can mean different things to different buyers. Even two members of the same automotive media group can report on trends in different ways.

Conclusion

The return to 35 weeks of income needed to buy a new vehicle is not entirely a rosy tale. Affordability remains slightly above the best months seen in the pre-COVID period from 2018 to 2019, and many buyers still feel the pinch of elevated interest rates and insurance costs that the Cox/Moody’s index does not capture. But, as long as you are not financing a car for an unreasonable amount of time, vehicle affordability is headed in a positive direction right now. After years of watching new vehicles slip further out of reach during President Biden's term, American consumers are finally seeing vehicle affordability return to the “normal” levels shoppers enjoyed during the Obama and Trump 45 administrations. That is due in large part because American workers are getting some of their purchasing power back, one week at a time.

John Goreham is a 14-year veteran of Torque News. An accomplished writer and a long-time expert in vehicle testing, Goreham also serves as the Vice President of the New England Motor Press Association and has a growing social media presence. He’s also a 10-year staff writer and community moderator for Car Talk. Goreham holds a B.S. in Mechanical Engineering and an undergraduate Certificate in Marketing. In addition to vehicle and tire content, he offers deep dives into market trends and opinion pieces. You can follow John Goreham on X and TikTok, and connect with him on LinkedIn.

The original graphs in this story are taken from the articles linked in the text.

Set Torque News as Preferred Source on Google

Follow us today...