As we move into 2026, a significant shift in risk assessment is catching thousands of light-truck owners off guard. Insurance carriers are leveraging transparency requirements by deploying AI-driven "Visual Risk Audits" during policy renewals. No longer relying on self-reporting, insurers are now using mandatory photo submissions and satellite imagery to identify aftermarket modifications, specifically suspension lifts, that deviate from factory safety specifications. This investigative report explores why a simple 2-inch lift is now leading to immediate policy cancellations and how owners can navigate this new "uninsurable" landscape.

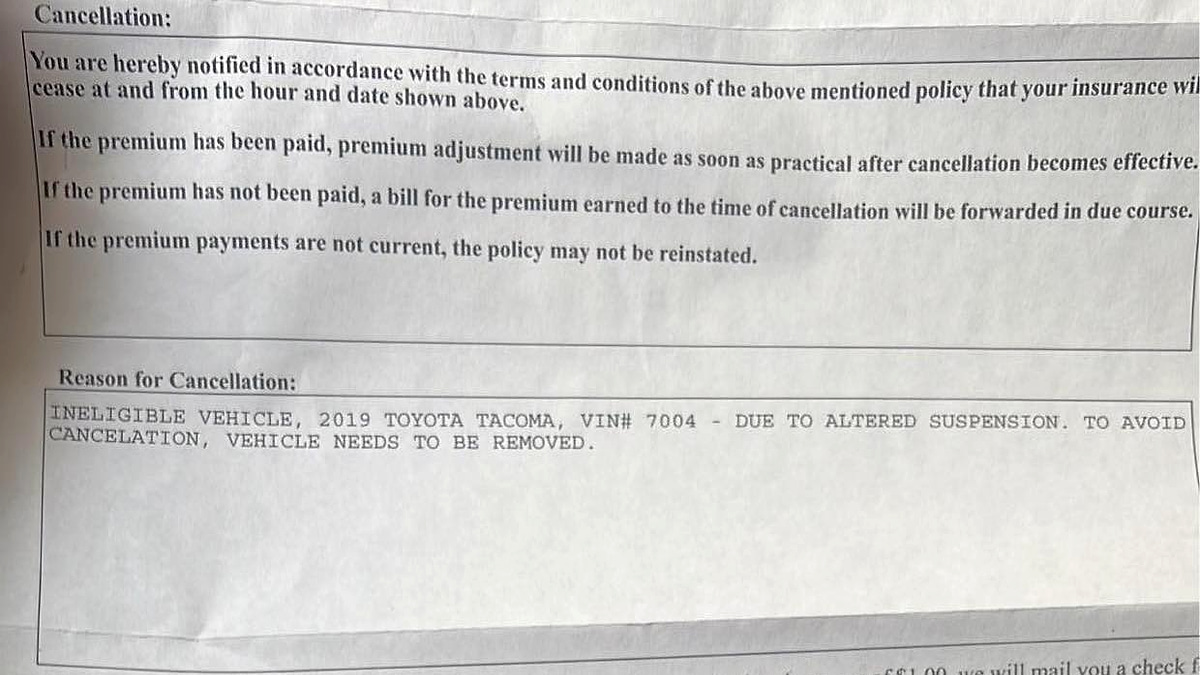

I have been covering the automotive industry for 30 years, and I have never seen a "quiet" policy shift move as fast as the one hitting truck country this month. If you drive a Toyota Tacoma in Texas, California, or the Rockies, you need to listen up because the rules of the game just changed. A Houston-based owner, Eriberto Soto, recently found out the hard way that his 2020 Toyota Tacoma is no longer "insurable" by his long-term carrier, simply because it sits a few inches higher than it did on the showroom floor.

Eriberto shared his experience on the Taco Nation Facebook page, stating:

"My insurance provider canceled the insurance on my 2020 Toyota Tacoma because it's lifted. They knew it was lifted because they asked for pictures of my truck when I had to renew my insurance. Has this happened to anyone else?"

From my view, this is not just an isolated incident; it's a calculated move by insurers to "trim their books" of modified vehicles that fall outside standard safety geometry. I recently reported that the 2025-2026 Tacoma TRD Pro carries over essentially unchanged; In that analysis, I noted that the TRD Pro’s factory-tuned suspension strikes a balance that insurers accept, but when owners go beyond those factory specs with aftermarket kits, they enter a "liability gray zone."

The "Why": Who Is Being Targeted and How?

You might be asking, "Why now?" The answer lies in the surge of AI-driven underwriting. According to a recent report by United Policyholders on the '16% Homeowner Trap', insurers are moving toward "micro-risk" modeling, using satellite imagery and mandatory photo audits to identify hazards before a human ever looks at a file. This technology has officially jumped from homeowners' insurance to auto policies.

When Eriberto’s insurer asked for photos, their algorithms weren't looking for scratches; they were measuring the gap between the tire and the fender. This matters because, as noted by Duncan Insurance in their 2025 legal insights, "enhanced liability coverage... promotes safer driving practices and better vehicle maintenance," and insurers now view any suspension modification as compromising a vehicle's Electronic Stability Control (ESC) and braking distance.

My Take

For decades, the unwritten rule among truck enthusiasts was that unless you had a massive accident, the insurance company didn't need to know about your 3-inch lift or your 35-inch tires. Those days are over. In my 30 years as a reporter and test driver, I've seen how even a slight change in ride height can affect a truck's "anchor" during a panic stop. I recently discussed this in my report on 4th Gen Tacoma 4WD limits, where I explained that "relying on tech instead of physics is a recipe for a totaled truck." Insurers have finally caught on to the physics.

What You Need To Know: The "Uninsurable" Checklist

I’ve compiled this analysis of the red flags insurers are looking for in March 2026:

- The 2-Inch Rule: Any lift exceeding 2 inches is now flagged for manual review by carriers like State Farm and Geico.

- Bumper Height Laws: If your front bumper is more than 28 inches above the ground, you may be in violation of state safety codes, giving the insurer a legal "out" to cancel your policy.

- Tire Diameter: Switching from a 31-inch to a 35-inch tire affects odometer and speedometer accuracy, which insurers view as a "material misrepresentation" if not disclosed.

- The "Photo Audit": If your renewal notice asks for four corner photos and an odometer reading, your policy is being audited by an AI risk-assessment tool.

Field Observations from Owner Communities

The technical feedback from the ground confirms that this isn't just a Texas problem. In a recent technical discussion on r/Insurance, one owner struggling with coverage for a modified Tacoma noted, "I probably have at least 20 grand into my truck and know in the event of a total loss I am probably going to take a loss on the majority of the aftermarket stuff," which you can read in the full Reddit thread here.

Another owner on r/Car_Insurance_Help highlighted how moving to a newer model doesn't solve the pricing issue, mentioning, "New Tacoma = way higher insurance than my Silverado... what am I missing?" This reflects the reality that newer trucks are more costly to repair due to advanced sensors that must be recalibrated after a lift. From my experience, if a lift kit isn't installed by a certified shop that can prove the ADAS (Advanced Driver Assistance Systems) was recalibrated, the insurer sees your truck as a "rolling liability."

From My View: A Specific Warning for 2026

If you are planning to modify a 2024, 2025, or 2026 Tacoma, you must be proactive. We are witnessing the end of an era where modifications were "invisible" to the front office. Insurers are now using the same high-resolution data to track vehicle thefts, which, interestingly, declined by 23% in 2025, to instead track "risk-prone" owners who have modified their vehicles.

Key Takeaways for My Readers

- Disclose Early: Do not wait for a photo audit. Call your agent and ask for a "Modified Vehicle Endorsement." It will cost more, but it prevents a mid-year cancellation.

- Stick to "Port-Installed" Options: Whenever possible, choose TRD lift kits installed by the dealer. These are typically covered under the factory warranty and are easier to insure because they appear on the original window sticker.

- Document Recalibration: Keep receipts proving your blind-spot monitors and pre-collision systems were recalibrated after the lift.

Don't Let a Satellite Photo Determine Your Future

The insurance landscape of 2026 is no longer about how well you drive; it is about how well your vehicle fits into a pre-defined safety box. For owners like Eriberto Soto, the "Taco" is more than just a truck; it's a lifestyle. But as insurance premiums are projected to jump another 8% this year, carriers are looking for any excuse to drop "non-standard" risks. My advice? Be your own advocate. Don't let a satellite photo or an AI algorithm decide your financial future.

It’s Your Turn

Has your insurance company asked for photos of your truck lately? Have you been hit with a "non-renewal" notice because of your mods? I want to hear your story. Tell us what you think! Leave a comment in the red "Add new comment" link below, and let’s get a discussion going. Your experience could help another owner avoid a total policy loss.

About The Author

Denis Flierl is a 14-year Senior Reporter at Torque News and a member of the Rocky Mountain Automotive Press (RMAP) with 30+ years of industry experience. Based in Parker, Colorado, Denis leverages the Rockies' high-altitude terrain as a rigorous testing ground to provide "boots-on-the-ground" analysis for readers across the Rocky Mountain region, California EV corridors, the Northeast, Texas truck markets, and Midwest agricultural zones. A former professional test driver and consultant for Ford, GM, Ram, Toyota, and Tesla, he delivers data-backed insights on reliability and market shifts. Denis cuts through the noise to provide national audiences with the real-world reporting today’s landscape demands. Connect with Denis: Find him on LinkedIn, X @DenisFlierl, @WorldsCoolestRides, Facebook, and Instagram.

Photo credit: Denis Flierl via Eriberto Soto

Set Torque News as Preferred Source on Google

Follow us today...

Comments

about time ive seen way…

Permalink

about time ive seen way worse suspenions very dangerous to other drivers and also displaying 6 headlights ...is that really necessary

Yeah and Jeeps lift kits and…

Permalink

In reply to about time ive seen way… by pj (not verified)

Yeah and Jeeps lift kits and suspension mods, tires sticking out past the wheel wells slinging mud and rocks at other vehicles. Lowered cars are dangerous as well. Busting shocks banging over bumps, scraping parking lots, slanted tires sticking our at unsafe angles. Low pro tires are dangerous blow and shred fast and easier and bad in weathered conditions. Squatted trucks. Sports cars excessively to fast making them un safe. Should have max limit to the max speed limit in the usa. Touch screens ard distractions and road hazardous.hid, leds, projectors are excessively bright, added light bars add to that. colored head light other than white us distracting. Along with christmas lights and neons. Tint windows darker the 20% to dark for safely driving at night. Excessive loud exhuast and horns scare and startle people. Causing accidents. This follows over to motorcycles. So same things apply. Rv and 5th wheel campers should be disallowed they dont fit on small backroads and damage peoples and public property including the rv/5 wheel. They are also top heavy wirh high roll over probability. Just unsafe vehicles. Every shoul drive the stock. For a safer on cost insurance effective society. Lol