The modern full-size truck market presents a deceptive financial illusion to unvouchered shoppers. While secondary market dynamics have triggered an aggregate 50% value drop on fourth-generation light-duty assets, hidden operational and financing structures systematically erode that apparent discount. A strict mathematical comparison reveals that a yawning gap in financing interest rates, coupled with localized structural updates to insurance premiums, can completely erode a $40,000 upfront purchase price advantage over a standard five-year amortization cycle.

This consumer advocacy report strips away showroom sales rhetoric to arm buyers with an actionable procurement strategy. By examining real-world auto loan interest rates, complex risk-rating variables, and geographic cost premiums, Torque News exposes the true cost of ownership. The following data-backed framework shifts the focus of acquisition from simple window-sticker prices to comprehensive, long-term asset-liability management.

The F-150 Financing Shock: How Interest Rates Erase Used Truck Savings

Our recent market deep dive revealed a historic valuation shift across full-size truck lines, explaining why 2021–2024 Ford F-150s lost 50% of their value compared to a new 2026 Lariat. While securing a premium pre-owned utility truck for half its original factory invoice price looks like an ironclad consumer win on paper, the underlying auto loan structures of the current credit environment tell a radically different story. Many buyers focus entirely on the vehicle's principal balance while remaining completely blind to the compound-interest penalties on used automotive assets.

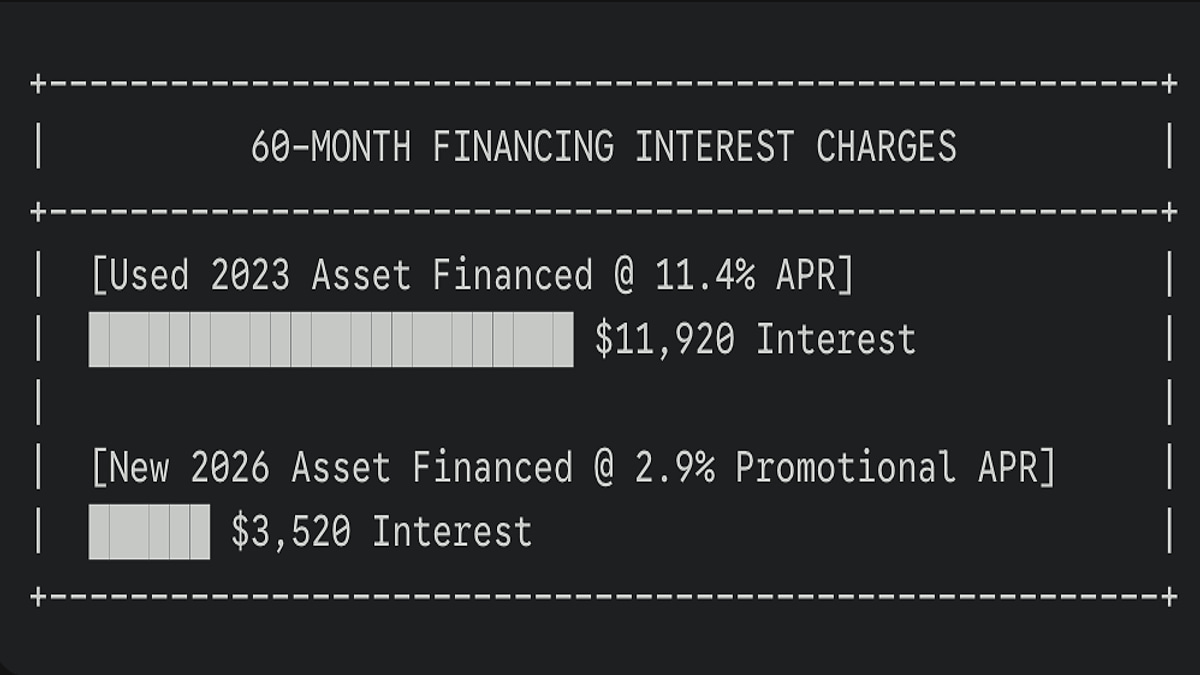

The credit landscape creates a massive penalty for secondary-market vehicles. According to the latest comprehensive credit data compiled by Experian's Automotive Finance Market analysis, the average interest rate for a new car loan hovers around 6.56%, whereas the average pre-owned vehicle interest rate sits at a steep 11.4% APR. When a consumer finances a heavily depreciated 2023 Ford F-150 Lariat with a principal balance of $37,250 over a standard 60-month term at an 11.4% tier-one rate, they incur $11,920 in pure interest charges.

Conversely, manufacturers routinely combat dealership inventory pileups by offering subsidized promotional financing on brand-new stock. If a buyer utilizes a factory-backed 2.9% promotional APR to finance a brand-new 2026 Ford F-150 Lariat showroom model, the total interest paid over that exact same five-year timeline drops significantly, shifting the ultimate financial calculus. This massive interest rate spread means the financing cost alone can quietly claw back a substantial portion of the pre-owned vehicle's upfront sticker discount.

The Hidden Underwriting Penalties on Advanced Automotive Electronics

Beyond the compounding interest payments, pre-owned truck shoppers face an invisible operational headwind from the commercial insurance underwriting sector. Modern fourth-generation F-150 variants are rolling supercomputers, packed with extensive safety sensor arrays, automated driving technologies, and multi-camera blind-spot systems. Actuarial data indicates that repairing these advanced technological components after an accident has driven standard collision claim costs to historic highs.

Insurance providers adjust their comprehensive premium matrices based on the age and out-of-warranty status of these complex electronic safety features. If a forward-facing radar module or a side-mirror blind-spot camera sensor fails or gets damaged on an older out-of-warranty truck, the repair bill requires specialized calibration tools that cost thousands of dollars. Actuarial reviews published by the Becker Friedman Institute for Economics confirm that as vehicle technology and parts complexity increase, property and casualty insurers aggressively scale up baseline premiums on older assets to counter the rising cost of minor property damage claims.

This premium inflation is felt acutely by truck owners operating in high-risk geographic areas. In our continuous coverage of Ford reliability, Torque News has tracked how regional weather anomalies alter consumer risk ratings. For example, a truck owner keeping an older out-of-warranty truck parked outdoors in the hail-prone Front Range corridors of Parker or Denver, Colorado, faces specialized geographic comprehensive premium surcharges. Because regional repair facilities demand premium labor rates to replace aluminum body panels and recalibrate exposed electronic safety sensors, regional insurance premiums for a used 2023 model can run $60 to $90 a month higher than a new 2026 model, which benefits from introductory low-risk rating tiers.

Consumer Action Plan: Mitigating the Used-Truck Capital Trap

For buyers determined to capitalize on the 50% drop in the secondary-market valuation without falling victim to high interest charges and insurance penalties, success requires following a strict, proactive procurement blueprint.

- Secure a guaranteed pre-approved auto loan from an independent credit union before setting foot inside a dealership showroom to avoid high dealer interest markups.

- Request a comprehensive, vehicle-specific insurance premium quote using the exact Vehicle Identification Number (VIN) to check for hidden technological or regional risk surcharges.

- Calculate the total cost of ownership over the entire planned loan duration, combining the principal balance, interest charges, insurance premiums, and expected out-of-warranty repair costs.

- Leverage the documented 50% depreciation metric during dealer negotiations to demand deep discounts on comprehensive extended service contracts that guard against transmission failures.

Evaluating the Alternative: When the 2026 Showroom Model Wins the Math

Understanding when to walk away from a pre-owned bargain and invest in a new vehicle comes down to checking for factory-backed financing. When major domestic manufacturers face rising inventory levels on dealership lots, they rarely cut the official MSRP. Instead, corporate offices funnel cash into highly effective promotional financing incentives.

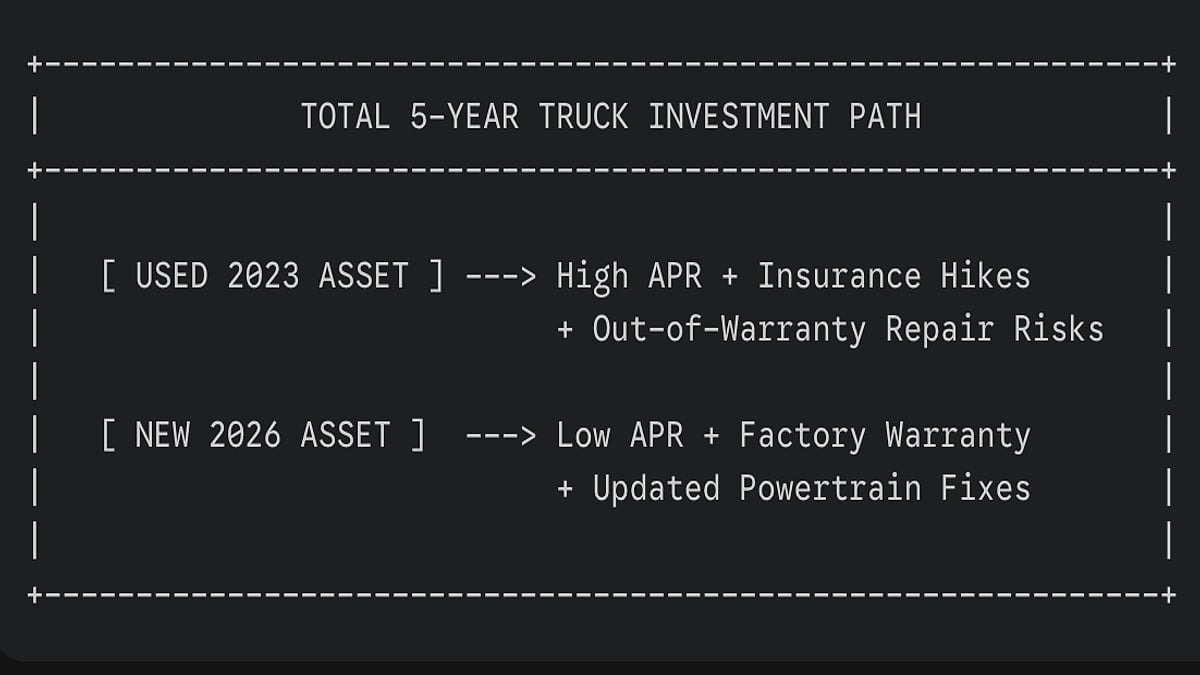

In my investigative tracking of factory fleet adjustments, I have seen how corporate finance programs can completely change the math on a new vehicle purchase. As documented in the Torque News advisory on F-150 powertrain selections, buyers who carefully align their vehicle choices with factory-backed structural updates can successfully avoid major out-of-pocket repair bills down the road. When a manufacturer combines a 0.9% or 1.9% promotional APR with a high-value trade-in incentive, the total cost of ownership curve for a brand-new 2026 model flattens, making it remarkably competitive with a high-interest used-vehicle loan.

Furthermore, a showroom-fresh 2026 model comes protected by a complete factory bumper-to-bumper warranty. This coverage removes the need to buy an expensive third-party extended service contract or keep a large cash reserve on hand for sudden mechanical emergencies. For truck owners who accumulate high mileage or use their vehicles for commercial towing, the peace of mind provided by factory warranty backing outweighs the apparent savings of a discounted but unprotected pre-owned vehicle.

Field Observations from Owner Financing Circles

Real-world financing experiences shared in active online truck communities highlight the real-world friction buyers face when trying to fund an older asset. Within popular online truck forums, everyday shoppers frequently share the exact loan terms and interest rate shifts they encounter at dealership finance desks.

On an active consumer finance thread within Reddit's r/whatcarshouldIbuy community, a pre-owned truck buyer detailed how a local lender's double-digit interest rate completely wiped out their hard-won vehicle discount, turning an affordable purchase into an expensive monthly burden. Additionally, detailed procurement reviews on Reddit's F-150 enthusiast boards note that buyers who skip a thorough pre-purchase inspection often end up with immediate maintenance costs that quickly erase any savings from a lower sticker price.

From over three decades of hands-on experience as an automotive industry consultant and technical advisor, these user experiences show exactly why total cost planning is so critical. When a buyer takes out an 11.4% auto loan to buy an out-of-warranty utility truck, they are essentially taking on a high-interest liability that requires flawless mechanical performance just to break even. The smart consumer looks past the initial discount and evaluates how the loan structure impacts their monthly household budget.

How Do You Safely Finance a Depreciated Truck?

If a truck buyer decides to capitalize on the 50% price drop and purchase a pre-owned 2023 F-150 Lariat, the next critical challenge is structuring the vehicle loan to avoid getting trapped in an upside-down equity position. Because early-generation post-pandemic trucks have shown volatile depreciation, taking out a long-term loan with zero down payment is a major financial risk. If the secondary market experiences another sudden value correction, an unprotected borrower can easily owe thousands of dollars more than the truck is actually worth.

To prevent this financial trap, smart buyers should follow a strict 20/4/10 budgeting rule. This strategy requires making a minimum 20% cash down payment, limiting the auto loan term to 48 months or less, and keeping total monthly transportation costs, including principal, interest, and insurance premiums, under 10% of gross household income. By keeping the loan term short and putting down a substantial initial investment, the buyer builds immediate equity in the vehicle. This protective equity buffer ensures that even if secondary-market valuations continue to slide, the owner remains financially secure and retains the flexibility to trade or sell the truck whenever they need to.

Consumer Verdict

Navigating today's complex automotive market requires looking beyond simple window-sticker prices and conducting a thorough total cost-of-ownership analysis. Capitalizing on a pre-owned F-150's 50% depreciation drop is an excellent way to avoid initial value loss, but only if you can bypass high used-car interest rates and localized insurance premium increases. If you have access to low-interest credit union financing or can pay cash, buying a pre-owned truck delivers an undeniable financial advantage. However, if you are forced to use standard dealership financing, the high interest charges on a used vehicle loan can quickly erase those upfront savings. Ultimately, running a comprehensive financial analysis that tracks every dollar spent on interest, insurance, and maintenance ensures you make a smart, defensive purchase that protects your long-term household budget.

Tell Us What You Think: Have you looked at financing rates for a used truck lately? Did high-interest charges or unexpected insurance costs push you toward buying a new showroom model instead? Please share your real-world loan terms, insurance quotes, and dealership experiences in the red Add new comment link below.

About The Author

Denis Flierl is a 14-year Senior Reporter at Torque News and a member of the Rocky Mountain Automotive Press (RMAP) with 30+ years of industry experience. Explore his full investigative reporting archives and technical guides at DenisFlierl.com. Based in Parker, Colorado, Denis leverages the Rockies' high-altitude terrain as a rigorous testing ground to provide "boots-on-the-ground" analysis for readers across the Rocky Mountain region, California EV corridors, the Northeast, Texas truck markets, and Midwest agricultural zones. A former professional test driver and consultant for Ford, GM, Ram, Toyota, and Tesla, he delivers data-backed insights on reliability and market shifts. Denis cuts through the noise to provide national audiences with the real-world reporting today’s landscape demands. Connect with Denis: Find him on LinkedIn, X @DenisFlierl, @WorldsCoolestRides, Facebook, and Instagram.

Photo credit: Denis Flierl

Set Torque News as Preferred Source on Google

Follow us today...