For over a decade, the primary barrier to electric vehicle (EV) adoption hasn’t been range anxiety or charging infrastructure—though those remain significant hurdles—it has been the "green premium." For the average consumer, the math simply didn’t work. You were asked to pay a 20% to 30% premium upfront for the promise of lower operating costs later. But that era just ended.

According to recent data, we have officially hit the Sub-Petrol Price Milestone. In several key markets, the average price of a new EV has officially undercut its internal combustion engine (ICE) equivalent. This isn't just a minor fluctuation; it is a fundamental shift in the tectonic plates of the automotive industry. Led by aggressive pricing strategies from brands like MG and Renault, the price parity we’ve been predicting for years has arrived early. Market data from April 2026 shows that in the UK, the average new EV price of £42,620 is now lower than the average petrol model at £43,405.

As someone who spends my time analyzing disruptive technology, I can tell you that when the "better" technology becomes the "cheaper" technology, the legacy tech enters a death spiral.

Where the Revolution is Winning (and Where It’s Stalled)

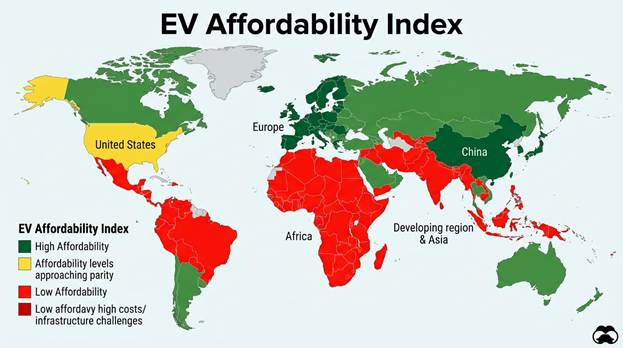

This phenomenon is most evident in Europe and China. In the UK, the Renault 5 E-Tech has become the poster child for this shift, topping buyer enquiry charts by offering iconic styling at a price point that challenges traditional hatchbacks. France has seen a similar surge, aided by social leasing programs that put EVs in reach of low-income households for as little as €100/month.

However, this parity has not yet materialized in the United States. While the Inflation Reduction Act provides tax credits, the "sticker price" of EVs in the U.S. remains high due to the American preference for massive SUVs and trucks. While a Renault 5 can achieve parity with a petrol car, a Ford F-150 Lightning still struggles to match the price of a base-model gas variant. Furthermore, protectionist tariffs on Chinese EVs are keeping the most affordable options out of the hands of American consumers, even as global battery pack costs have dropped toward the elusive $80/kWh mark.

Winners and Losers of the Price War

The countries likely to benefit the most from this trend are those with high urban density but limited domestic oil reserves. Nations like Japan, South Korea, and much of the European Union will see a massive improvement in their balance of trade. China, currently producing the vast majority of EVs sold globally, stands to gain the most as it moves from a manufacturing hub to a global brand powerhouse.

Conversely, the "losers" will be oil-dependent economies and nations with weak electrical grids. In parts of Africa and Southeast Asia, the lack of a stable "last mile" power grid makes the affordability of the vehicle irrelevant. These regions risk becoming the "dumping ground" for the world’s remaining ICE production, potentially locking them into older, more expensive energy dependencies for decades.

The 2030 Market Mix: A Fragmented Future

By the end of the decade, the automotive world will not be a monolith. We are moving toward a highly fragmented market mix:

- Pure EV (45%): Dominant in urban environments.

- EREV (Extended Range Electric Vehicles) (20%): This is the "sleeper" category. Expected to see significant growth through 2033, EREVs offer a pragmatic bridge for those who need long-distance flexibility.

- Hybrid (20%): The "new normal" for entry-level vehicles.

- ICE (15%): Reserved for heavy-duty industrial use and enthusiast "toy" cars.

The most terrifying prospect for current car owners is the projected collapse of ICE resale values. As EVs become cheaper to buy and run, the secondary market for petrol cars will likely crater. Analysts suggest that second-hand ICE prices could fall exponentially as they are shunned by used-market buyers concerned with future fuel costs and urban bans.

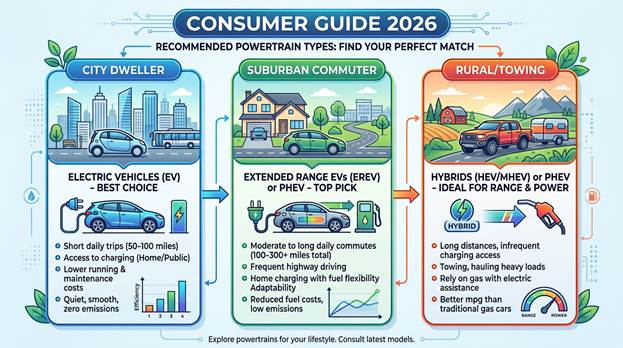

Regional Buying Recommendations for 2026

If you are looking at a new vehicle for 2026, your strategy must be dictated by your geography:

- Europe/UK: Buy a pure EV. The infrastructure is there and the average price now favors electric. The Renault 5 or MG S5 are the current value leaders.

- North America: If you are a multi-car household, at least one vehicle should be a pure EV. For your primary long-haul vehicle, look at an EREV or a Plug-in Hybrid (PHEV) to protect your resale value while charging infrastructure catches up.

- Asia-Pacific/Emerging Markets: Focus on EREVs and Hybrids. In regions like India and ASEAN nations, EREVs are the fastest-growing segment due to infrastructure gaps.

Wrapping Up

The sub-petrol price milestone is the "iPhone moment" for the automotive industry. It signals that the transition is no longer a matter of environmental policy, but of simple economics. When MG and Renault proved they could underprice petrol, they started a clock that cannot be stopped. For the consumer, 2026 represents the last "safe" year to navigate this transition before the market significantly devalues internal combustion. The smart money is moving to electrons—not just because it’s better for the planet, but because it’s finally better for the wallet.

Disclosure: Images rendered by Artlist.io

Rob Enderle is a technology analyst at Torque News who covers automotive technology and battery developments. You can learn more about Rob on Wikipedia and follow his articles on TechNewsWord, TGDaily, and TechSpective.

Set Torque News as Preferred Source on Google

Follow us today...